Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Do Buyers Need an Appraisal in San Francisco?

Do Buyers Need Their Own Appraisal in San Francisco Real Estate?

Author: Ms. San Francisco Real Estate | Last Updated: March, 2026

The San Francisco housing market moves fast. Because of this, homebuyers often ask a key question. Do they need a separate appraisal when buying a home?

The short answer is: it depends. First, buying a property does not always require an extra appraisal. However, it is a smart choice in certain situations. In fact, knowing when you need one can save you both money and stress. Therefore, talk to a local real estate expert. They can help you decide based on your goals, your loan, and your chosen neighborhood.

Understanding Home Appraisals in San Francisco, CA

First, let’s define what an appraisal is. It is a professional check of a home’s fair market value. An objective, licensed appraiser does this work. Furthermore, in a complex market like SF, they look at several key details:

-

Recent sales: They look at similar homes nearby (called “comps”).

-

Home condition: They check for repairs and new updates.

-

Location details: They note features like good schools or transit.

-

Market trends: They look at current SF real estate trends.

Most of the time, mortgage lenders order these appraisals. Even so, homebuyers always have the right to request their own.

When a Buyer May Not Need Their Own Appraisal

Usually, if you have a loan, you do not need an extra appraisal. This is true because:

-

The lender takes care of it: Banks require this before giving you a mortgage.

-

It protects the lender: It ensures the loan is not larger than the home’s worth.

-

It is easier: The cost is already part of your closing fees.

As a result, a standard lender appraisal usually meets all your needs in San Francisco.

When Buyers Should Consider an Independent Appraisal

On the other hand, SF real estate can be tricky. Because of this, getting your own appraisal is often a smart move. For example, you should consider one if you are:

-

Paying with all cash: Lenders are not involved to order one for you.

-

Buying a unique home: Standard sales data might not reflect its true value.

-

Looking in a changing market: Prices might be shifting week by week.

-

Worried about paying too much: Especially during a bidding war.

-

Buying directly from the owner (FSBO): Owners often set prices based on emotion.

-

Taking over an inherited home: The home’s history might be unclear.

In these cases, a local SF real estate agent can help. They will tell you if the extra cost is worth it.

Cash Buyers and Appraisals in SF

Cash buyers do not legally need an appraisal. However, many smart buyers still choose to get one. For instance, the benefits include:

-

Checking the true value before spending your cash.

-

Getting more power to lower the price.

-

Protecting the future value of your new home.

Furthermore, an agent might suggest a pre-sale appraisal in high-end areas. These include Russian Hill, Noe Valley, or Pacific Heights. As a result, you can feel totally confident about the price.

Neighborhood Spotlights: Why Appraisals Matter More in SF

Property values change a lot across San Francisco. In fact, they can change from block to block. Therefore, appraisals are very important in neighborhoods with:

-

Mixed housing: Areas with both apartments and houses.

-

Low sales: Quiet streets where homes rarely sell.

-

Changing prices: Areas that are growing very fast.

For example, places like the Mission District or SoMa need careful pricing. The same is true for Bernal Heights and the Sunset District. An online tool simply cannot do this well.

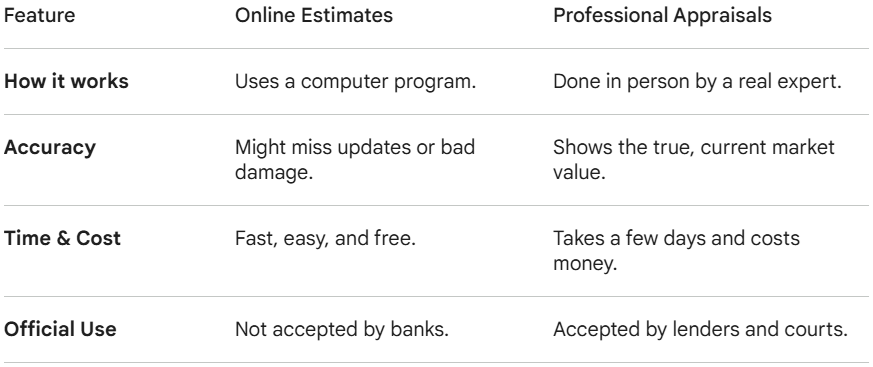

Professional Appraisals vs. Online Estimates

Many buyers use online tools to guess a home’s value. However, these tools have big limits in a diverse city like SF.

Therefore, a real estate agent is your best resource for understanding these numbers.

How Appraisals Affect Financing and Negotiations

Appraisals are not just paperwork. In fact, they are vital tools for:

-

Getting loan approvals: Lenders will not fund more than the home is worth.

-

Protecting your deposit: You can back out if the home is worth less than the price.

-

Lowering the price: You can use the data to negotiate.

What happens if an appraisal comes in low? First, you can accept the price and pay the difference. Second, you can try to lower the price with the seller. Finally, you can just walk away from the deal.

Final Thoughts: Is an Independent Appraisal Worth It?

In conclusion, getting your own appraisal can lead to better results. Yet, the final choice depends on a few things. These include your loan type, the home itself, and the current market. Ultimately, working with an experienced SF agent keeps you informed. Thus, you can easily decide if an extra appraisal is right for you.

FAQs: Buyer Appraisals in San Francisco Real Estate

Q: When is an appraisal strictly required?

A: If you use a mortgage, you must have an appraisal. The bank requires it. As a result, the lender orders it, but you pay for it at closing.

Q: Should cash buyers get an appraisal?

A: It is completely optional. However, it is highly recommended for unique SF homes. Typically, the cash buyer pays for this service.

Q: Can I just rely on online home value estimates?

A: Online estimates give you a rough idea. However, they cannot replace a real pro. Therefore, use a licensed appraiser or an agent for an accurate price.

Q: How can I find a reliable San Francisco real estate agent?

A: Look for an agent with great reviews. Also, make sure they have plenty of experience selling homes right here in San Francisco.

Need Expert Advice in the SF Market?

The right real estate agent makes all the difference. For instance, knowing exactly when to order an extra appraisal can save you thousands. So, are you ready to buy with confidence? Reach out to Ms. San Francisco Real Estate today to start your journey!

How Realtors Use AI for Faster Property Valuation in SF

How Realtors Can Use AI Tools for Faster Property Valuation

Author: Ms. San Francisco Real Estate | Last Updated: March, 2026

The San Francisco real estate market is highly data-driven. Furthermore, it moves extremely fast. Therefore, buyers and sellers expect quick, accurate answers. Specifically, they want to know a home’s exact value immediately.

Consequently, artificial intelligence is helping real estate agents deliver faster evaluations. While these tools give professionals a huge advantage, they do not replace human expertise. Ultimately, the best results come from combining deep local knowledge with advanced technology.

Here is a structured overview of how realtors use AI to price homes smarter and faster.

Why Speed Matters in San Francisco Property Valuation

First, delays in pricing feedback can hurt your sale. Specifically, in competitive neighborhoods like the Sunset District, SOMA, Noe Valley, and Pacific Heights, slow responses cause problems.

For example, delays can lead to:

- Missed buyer interest.

- Lower offer amounts.

- Longer time on the market.

As a result, San Francisco real estate professionals use advanced data systems. Ultimately, this helps them process sales information instantly while monitoring real-world trends.

What AI Tools Do for Real Estate Agents

Next, modern AI valuation tools analyze property data in seconds. Consequently, they help agents make faster, more informed decisions.

Typically, these tools assess:

- Recent San Francisco homes for sale.

- Comparable sales by ZIP code.

- Market demand and supply.

- Property size, age, and layout.

- Local appreciation trends.

Therefore, agents can prepare highly effective listing presentations and buyer consultations.

⚖️ AI vs. Appraisals: Understanding the Difference

Moreover, many people confuse automated valuations with professional appraisals. However, these are two very different tools. Below is a quick comparison of how they function.

Ultimately, a top San Francisco real estate agent knows when to use AI. Furthermore, they know exactly when to recommend a certified home appraiser in San Francisco.

Neighborhood Spotlights: Where AI Needs Human Insight

Additionally, San Francisco consists of many complex micro-markets. Because of this, property values change wildly from block to block.

Consequently, AI tools often struggle with:

- Historic homes.

- Mixed zoning areas.

- Condo and single-family overlaps.

For instance, human expertise is especially important in:

- Mission District.

- Castro.

- Bernal Heights.

- Russian Hill.

Thus, a knowledgeable professional is essential to interpret AI data correctly.

How AI Helps Home Sellers and Buyers

On one hand, AI tools help real estate agents identify overpricing risks early. Furthermore, they support pricing discussions with hard data. As a result, sellers can adjust their strategies quickly to match shifting market conditions.

On the other hand, AI also protects buyers. Specifically, it helps them compare San Francisco condos and evaluate listing prices. Therefore, buyers can spot pricing gaps and negotiate stronger deals without overpaying.

AI in Mortgage, Refinance and Cash Offers

Furthermore, AI valuation tools support the financial side of real estate.

Specifically, they help with:

- Mortgage appraisal preparation.

- Refinance evaluations.

- Cash offer analysis in San Francisco, CA.

- Investor purchase modeling.

Nevertheless, pricing accuracy must still be confirmed by licensed professionals and lenders.

❓ FAQs: AI and Property Valuation in San Francisco

Are AI-based valuations accurate in the San Francisco Bay Area? Sometimes. However, accuracy depends heavily on data quality, neighborhood complexity, and property condition.

Can AI replace home appraisals? No. Specifically, certified appraisals are still legally required for lending and financial purposes.

Should sellers rely only on AI pricing tools? No. Instead, AI tools work best when they support the guidance of an experienced real estate agent.

What is the best way to price my San Francisco home? Consult a licensed San Francisco real estate agent. Ultimately, they understand local market trends and use technology strategically.

🏡 Ready to Price Your Home Smarter? Let Ms. San Francisco Real Estate Help

Technology has made property valuation faster, but accuracy still depends on expert interpretation. Therefore, AI tools are only as reliable as the professionals using them.

Ms. San Francisco Real Estate combines cutting-edge AI technology with decades of hands-on local experience. Whether you are selling a historic home in the Castro or buying a modern condo in SOMA, we know how to translate complex data into real-world profit. Ultimately, we ensure you get the best possible price without the guesswork.

Do not leave your home’s value up to an algorithm. Contact Ms. San Francisco Real Estate today for a fast, accurate and data-driven property valuation!

The Future of AI-Powered Home Valuation in San Francisco

The Future of AI-Powered Home Valuation in San Francisco

Author: Ms. San Francisco Real Estate | Last Updated: March, 2026

The San Francisco real estate market moves incredibly fast. Today, it is evolving faster than ever due to new technology. Specifically, automated home valuation systems are completely reshaping the local housing market.

As a result, artificial intelligence (AI) is transforming how we buy and sell property. Therefore, agents, buyers, and sellers can now make smarter decisions using instant data. However, in a highly competitive market, you must understand both the strengths and limits of these tools.

Here is a clear breakdown of how AI is changing San Francisco real estate.

What Is AI-Powered Home Valuation?

First, AI-powered home valuation relies on Automated Valuation Models (AVMs). Essentially, these tools use complex math to analyze massive amounts of property data in seconds.

For example, they look closely at:

- Recent San Francisco home sales.

- Comparable properties by ZIP code.

- Neighborhood market trends.

- Supply and demand conditions.

- Property size, condition, and recent upgrades.

- Current economic indicators and interest rates.

While online estimates give a helpful starting point, they are not perfect. Ultimately, they do not provide a complete picture of your San Francisco home’s true market worth.

Why AI Matters in San Francisco

Next, San Francisco has one of the most complex housing markets in the country. In fact, property values can change drastically from one street to the next.

Therefore, AI adds massive value by:

- Analyzing real estate trends in real time.

- Spotting underpriced or overpriced properties quickly.

- Helping investors find great San Francisco investment opportunities.

- Supporting faster pricing decisions for busy sellers.

Nevertheless, AI only processes raw data. Consequently, unique home features and local neighborhood vibes still require a human expert.

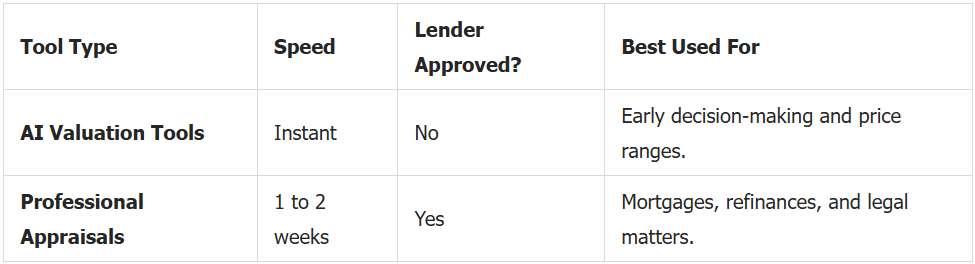

⚖️ AI vs. Human Expertise: What’s the Difference?

To clarify, AI systems and human experts both bring unique strengths to the table. Below is a quick comparison of how they differ.

Ultimately, the smartest approach is to use both. Indeed, a hybrid strategy gives you the absolute best financial results.

Neighborhoods Where AI Struggles Most

Furthermore, AI valuation tools often fail in certain areas. Specifically, they struggle with unique architecture, varied demand, or limited sales data.

For instance, AI often misprices homes in:

- Pacific Heights.

- Noe Valley.

- Mission District.

- Sunset and Richmond Districts.

- SOMA loft conversions.

Because these San Francisco neighborhoods are so unique, a local agent is absolutely essential for accurate pricing.

How AI Changes Buying and Selling

Additionally, AI is shifting the entire transaction process for everyone involved.

For Home Buyers: First, AI helps buyers track homes for sale and compare prices easily. However, a skilled San Francisco real estate agent protects buyers from overpaying.

For Home Sellers: Meanwhile, AI helps sellers estimate listing prices and evaluate cash offers. Still, pairing this data with an experienced agent guarantees stronger negotiations and access to serious buyers.

AI, Appraisals and Financing

Moreover, AI is changing mortgage appraisals and lender risk analysis. While these tools speed up the loan process, human appraisers remain vital.

Specifically, you still need a certified appraiser in San Francisco for:

- FHA and VA loans.

- Probate and trust sales.

- Investment properties.

In short, computers cannot replace the judgment of a licensed valuation professional.

❓ FAQs: AI-Powered Home Valuation in San Francisco

Are AI home valuations accurate in San Francisco? Sometimes. However, accuracy varies wildly based on the neighborhood, property condition, and available data.

Can AI replace a real estate agent? No. Specifically, agents provide negotiation skills and buyer psychology insights that AI simply cannot replicate.

Do I need an independent valuation of my property? Yes. Indeed, professional appraisals are often legally required for selling, refinancing, and probate matters.

🏡 Ready to Find Your Home’s True Value?

AI tools are a great starting point, but you should never let a robot have the final say on your biggest financial asset. Therefore, if you want to know exactly what your home is worth, it is time to partner with a local expert.

Ms. San Francisco Real Estate uses the latest AI technology alongside decades of hands-on human experience. Whether you are buying, selling, or investing, we understand the hyper-local trends that algorithms miss. Ultimately, we ensure your home is priced perfectly so you never leave money on the table.

Stop guessing your property’s value. Contact Ms. San Francisco Real Estate today for a highly accurate, data-driven home valuation!

Selling a House As Is in San Francisco: What to Expect

Selling a House “As Is” in San Francisco: What to Expect

Author: Ms. San Francisco Real Estate | Last Updated: March, 2026

Selling a house “as is” in San Francisco can be a great choice. For instance, it is perfect for homeowners who want a fast, easy sale. Additionally, if you are dealing with an inherited property, this route saves valuable time. Therefore, understanding how as-is sales work helps prevent you from losing money.

In fact, many San Francisco sellers get great results this way. Specifically, they work with a real estate agent who knows cash-sale strategies. Ultimately, this helps them sell homes quickly without doing any repairs.

Here is a breakdown of what you need to know about selling your home as is.

What Does “As Is” Mean in Real Estate?

First, selling a home “as is” means you will not make repairs before closing. However, this does not mean you can hide known problems.

Instead, California law still requires sellers to:

- Disclose all known defects in the home.

- Provide required transfer and hazard papers.

- Allow buyers to inspect the property.

Consequently, a smart San Francisco real estate agent is highly valuable. Indeed, they help you sell your home legally while following all state rules.

Why Homeowners Choose to Sell As Is

Next, you might wonder why people skip repairs. Generally, many homeowners choose to sell as is for these reasons:

- Costly or outdated home repairs.

- Inherited or probate properties.

- Rental homes with heavy tenant damage.

- Pre-foreclosure or sudden money problems.

- Relocation or very tight timelines.

- Investor or cash-offer opportunities in San Francisco, CA.

As a result, even as-is homes in good neighborhoods can attract multiple offers.

San Francisco Market Trends for As-Is Homes

Furthermore, the San Francisco real estate market loves as-is properties. Specifically, there is strong demand for:

- Fixer-uppers in prime locations.

- Investment properties.

- Condos and houses priced below normal retail value.

For example, neighborhoods with high as-is activity include:

- Bayview–Hunters Point.

- Outer Mission.

- Visitacion Valley.

Meanwhile, real estate investors and cash buyers are always looking for homes here.

Pricing an As-Is Home Correctly

Moreover, accurate pricing is critical when selling a home as is. Otherwise, you might leave thousands of dollars on the table.

Therefore, to find fair market value, you should look at:

- Recent sales of similar homes nearby.

- Property condition and estimated repair costs.

- Buyer demand in your specific neighborhood.

- A professional home appraisal in San Francisco, CA.

Although online tools give a rough guess, they are not perfect. Thus, only a licensed appraiser or local agent can give an exact price.

Who Buys As-Is Homes in San Francisco?

Additionally, as-is homes attract a specific type of buyer.

Typically, you will hear from:

- Cash home buyers in San Francisco, CA.

- Local real estate investors.

- Contractors and property flippers.

- Buyers looking for a fun renovation project.

In most cases, cash buyers close much faster. However, they usually expect a lower price in exchange for that speed.

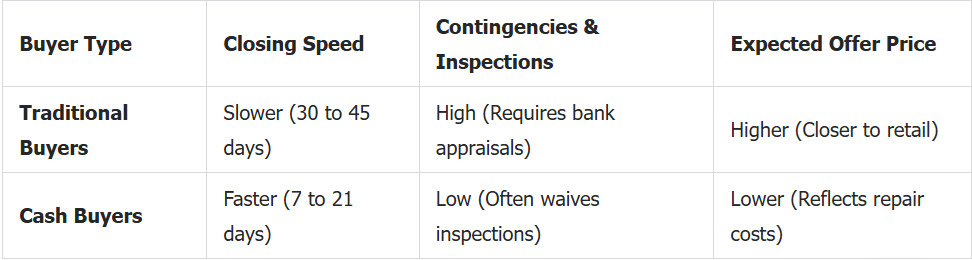

⚖️ Traditional Sale vs. Cash Sale: What to Expect

To clarify, it helps to compare your selling options directly. Below is a simple breakdown of what to expect from each buyer type.

Ultimately, an experienced San Francisco real estate agent can help you pick the best path. Indeed, they focus on your best financial outcome, not just a fast sale.

Do You Still Need an Appraisal?

Surprisingly, an appraisal is highly recommended even for as-is sales.

Specifically, a San Francisco home appraisal helps:

- Protect you against pricing your home too low.

- Support your side during price negotiations.

- Compare cash offers to normal retail pricing.

- Clarify the home’s true market value.

Because of this, many sellers request a pre-sale valuation before listing.

❓ FAQs: Selling a House As Is in San Francisco

Can I sell my house as is without a realtor in San Francisco? Yes. However, the process involves complex pricing, deals, and legal papers. Consequently, many private sellers accidentally undervalue their homes.

Will buyers still inspect an as-is home? Yes. To clarify, “as is” means no repairs are required. However, it does not mean inspections are skipped.

Can I sell as is during foreclosure or probate? Absolutely. In fact, many San Francisco house buyers specialize in foreclosure and probate sales.

Do as-is homes sell for less? They can. Nevertheless, careful pricing and proper marketing will minimize any unnecessary price drops.

🏡 Ready to Sell? Let Ms. San Francisco Real Estate Help

Selling your home “as is” should relieve your stress, not add to it. Therefore, if you want to skip the repairs but still maximize your profit, you need an expert on your side.

Ms. San Francisco Real Estate knows exactly how to market as-is properties. Whether you need a lightning-fast cash buyout or want to attract competitive investors, we handle all the heavy lifting. Ultimately, we protect your equity and ensure a smooth, legal closing.

Do not settle for a lowball offer. Contact Ms. San Francisco Real Estate today to discover the true value of your as-is property!

How to Sell Your House Without a Realtor in San Francisco (FSBO Guide)

How to Sell Your House Without a Realtor in San Francisco: Step-by-Step

Author: Ms San Francisco Real Estate | Last Updated: February, 2026

You can definitely sell your San Francisco house without a real estate agent. In fact, this is called “For Sale By Owner” or FSBO. However, it takes time, local market knowledge, and good planning.

For instance, many homeowners want to sell fast for cash to skip large agent fees. Meanwhile, others want to sell their home “as-is” to local investors. Therefore, before you put a sign in your yard, you need to know exactly how the process works. Ultimately, this protects your money and your time.

Here is a simple guide to selling your home on your own.

Step 1: Know the San Francisco Market

First, before you list your home, you must know what buyers want. Additionally, you need to know what similar homes cost.

Specifically, look at these key facts:

- Recent home sales in your neighborhood.

- How long homes stay on the market.

- What buyers are willing to pay right now.

- How many other homes are for sale.

San Francisco is a fast-paced market. As a result, home prices change from block to block. Because of this, even people selling on their own often ask a local expert for advice.

Step 2: Find Your Home’s True Value

Next, pricing your home wrong is a big risk. For example, if the price is too high, buyers will walk away. On the other hand, if it is too low, you lose money.

Therefore, here is how to find the right price:

- Pay for a professional home appraisal in San Francisco, CA.

- Look at the final sale prices of similar homes nearby.

- Get a price estimate from a local real estate pro.

Online tools are a good start. Still, do not rely on them alone to price your home.

Step 3: Get Your Home Ready to Sell

Furthermore, you must make your home look great to attract normal buyers.

To do this, focus on these simple steps:

- Clean deeply and clear out the clutter.

- Fix small things like leaky faucets and chipped paint.

- Make the outside of your house look inviting.

- Check that the heater, plumbing, and lights work well.

Otherwise, unless you are selling “as-is” to an investor, buyers expect a move-in ready home.

Step 4: Market Your Home Well

Moreover, without an agent, you must find the buyers yourself. Indeed, a simple yard sign is not enough.

Instead, try these marketing ideas:

- Pay for bright, professional photos.

- Put your home on FSBO websites.

- Share your listing on Facebook, Instagram, and Nextdoor.

- Post in local San Francisco housing groups.

Step 5: Talk to Buyers and Make a Deal

Soon after, you will start hearing from people who want to buy.

For instance, you might meet:

- Normal buyers who need a bank loan.

- Local real estate investors.

- Companies that buy houses for cash in San Francisco, CA.

Consequently, be ready to do the following:

- Check their bank proof or loan letters.

- Compare fast cash offers with higher loan offers.

- Agree on the final price, repair rules, and closing dates.

Step 6: Handle the Legal Paperwork

Additionally, California has strict laws about selling houses. Specifically, you must tell buyers about any known problems with the home.

Therefore, you will need to fill out:

- Transfer Disclosure Statement (TDS).

- Natural Hazard Disclosure (NHD).

- Lead-Based Paint form (for homes built before 1978).

- Purchase contracts and escrow papers.

Unfortunately, mistakes in these papers can cost you money. Thus, it is smart to hire a real estate lawyer or a paperwork expert to help you.

Step 7: Close the Sale

Finally, after you accept an offer, you reach the final steps.

Specifically, this part includes:

- Opening an account with a local title company.

- Letting the buyer inspect the home.

- Fixing any sudden problems with the property title.

- Signing the final papers and handing over the keys.

In the end, many sellers choose cash buyers for a fast, easy close. However, just remember that cash offers are often a little lower than normal offers.

⚖️ When FSBO Makes Sense (and When It Doesn’t)

In summary, selling on your own is a good idea if:

- You already know who is buying the house.

- You are selling directly to a cash buyer.

- You care more about a fast sale than getting top dollar.

Nevertheless, keep in mind that a good San Francisco agent can often get you more money. Ultimately, their marketing and deal-making skills usually cover the cost of their fee.

❓ FAQs: Selling a House Without a Realtor in San Francisco

Can I sell my house without a realtor in San Francisco, CA? Yes. However, you must handle the pricing, marketing, deals, and legal papers yourself.

Do cash buyers need a home appraisal? Usually, no. Instead, banks need appraisals, not cash buyers. Still, getting one yourself can help you set a fair price.

How fast can I sell my home in San Francisco? Cash sales can close in just 7 to 14 days. Meanwhile, normal sales with a bank loan take 30 to 45 days.

Is it cheaper to sell without an agent? You do save on the agent’s fee. However, pricing mistakes or bad deals can cost you much more than that fee.

🏡 Ready to Sell? Let Ms. San Francisco Real Estate Help

Selling a home on your own is a massive undertaking. Therefore, if you want to skip the stress, avoid costly legal mistakes, and maximize your final sale price, it is time to bring in an expert.

Ms San Francisco Real Estate knows the Bay Area market inside and out. Whether you need a fast, hassle-free sale or want to list traditionally to get top dollar, we have the network, marketing power, and negotiation skills to make it happen smoothly.

Do not leave your hard-earned equity on the table. Contact Ms San Francisco Real Estate today for a free, no-obligation home valuation and discover exactly how much your home is worth!

How to Prepare for a Home Appraisal in San Francisco (2026)

How to Prepare for a Home Appraisal in San Francisco

Author: Ms San Francisco Real Estate | Last Updated: February, 2026

Currently, the San Francisco market is competitive. Whether selling or refinancing, the appraisal is critical. Therefore, preparation is not optional. In fact, a messy home can lose you money. Conversely, a prepped home attracts top dollar.

Basically, the appraiser acts as the judge. If they see value, the loan gets approved. However, if they don’t, the deal can die. Fortunately, Ms. San Francisco Real Estate is here. Below is your step-by-step guide for 2026.

🧐 1. Why Appraisals Matter

First, understand the goal. Technically, an appraisal is an unbiased opinion of value. Crucially, lenders require it to protect their cash.

Common reasons for appraisals:

- Sales: To confirm the purchase price.

- Refinance: To lower your interest rate.

- Divorce: To split assets fairly.

- Cash Offers: To verify the investment potential.

Ultimately, the appraiser looks at the data. So, you must provide the best evidence.

🏘️ 2. Know Your Market (Step 1)

Before the appraiser arrives, study the neighborhood. In San Francisco, prices change by the block. Therefore, generic tools often fail.

What to analyze:

- Comps: Specifically, look at recent sales nearby.

- Trends: Currently, are prices rising or falling?

- Inventory: If supply is low, value goes up.

A local agent helps you interpret this. Thus, you are armed with facts.

🛠️ 3. Smart Improvements (Step 2)

Surprisingly, you don’t need a full renovation. Instead, focus on high-ROI fixes. Appraisers look for “effective age,” not just luxury.

Consequently, minor repairs yield major returns. So, fix the faucet before listing.

🧹 4. The Deep Clean (Step 3)

Visibly, clutter shrinks a room. Although appraisers try to look past it, they are human. Therefore, a clean home scores higher.

Your Pre-Appraisal Checklist:

- Declutter: Clear all countertops.

- Clean: Deeply scrub the bathrooms.

- Access: Ensure the attic and garage are open.

- Pets: Ideally, remove them for the visit.

Also, document your upgrades. If you replaced the roof, prove it. Provide a list of improvements and dates. This makes the appraiser’s job easier.

📍 5. Sell the Location (Step 4)

Undeniably, location drives value in SF. However, an appraiser might miss the nuances. So, leave a note highlighting the perks.

Mention these assets:

- Transit: Proximity to BART or Muni.

- Lifestyle: Walkability to parks and cafes.

- Schools: Access to top-rated education.

Even similar homes vary by district. For example, Noe Valley differs from Mission Bay. Thus, context is everything.

⚡ 6. Special Situations (Step 5)

Sometimes, the sale is complex. In 2026, cash offers are common. Even then, value matters.

Scenarios requiring extra care:

- Inheritance: Often, these homes need work.

- Divorce: Here, neutrality is key.

- Foreclosure: Speed is the priority.

In these cases, an experienced agent is vital. We coordinate with the appraiser to ensure fairness. Consequently, the process moves fast.

❓ FAQs: SF Appraisals

How much does it cost? Typically, between $400 and $700. It depends on the size.

Is the Zestimate accurate? Rarely. It misses local nuances. Always trust a human appraiser.

Should I get a pre-listing appraisal? Yes. Especially for unique or luxury homes. It helps set the right price.

Do cash buyers need appraisals? Not always. However, they use them to verify value.

Final Thoughts

In summary, preparation pays off. Ultimately, you control the condition of the home. Ms. San Francisco Real Estate helps you control the narrative. So, contact us today to get started.

Top 6 Factors Influencing Your San Francisco Home Value (2026)

Top Factors That Influence Your San Francisco Home Value Estimate

Author: Ms San Francisco Real Estate | Last Updated: February, 2026

Currently, San Francisco real estate is complex. In 2026, buyers are picky. Therefore, accurate valuation is vital. Whether selling or refinancing, you need data. Specifically, you must know what drives the price.

Basically, an estimate is not a guess. Instead, it is a calculation. Appraisers look at specific traits. Below is a breakdown of the top factors.

📍 1. Location, Location, Location

Undoubtedly, this is the biggest factor. In San Francisco, the neighborhood dictates the baseline. For example, a home in Pacific Heights costs more than one in the Outer Sunset.

Key location drivers include:

- Prestige: Specifically, areas like Nob Hill command premiums.

- Transit: If you are near BART, value rises.

- Walkability: Also, proximity to parks and cafes matters.

Consequently, the zip code sets the stage. Then, the house plays its part.

📐 2. Property Size and Layout

Next, size matters. However, it is not just about square footage. Crucially, the layout must flow.

What buyers look for:

- Bedrooms: Generally, more rooms mean more money.

- Flow: Ideally, the floor plan feels open.

- Outdoor Space: In SF, a yard is gold.

Surprisingly, a small home with a good layout often beats a large, awkward one. Thus, usability is key.

🛠️ 3. Condition and Upgrades

Visibly, the condition impacts the first impression. Appraisers look past the decor. Instead, they check the “bones.”

Therefore, deferred maintenance hurts you. Conversely, smart upgrades pay off. So, fix the leaks before listing.

📊 4. Market Trends & Economy

Constantly, the market shifts. In 2026, economic factors play a huge role. Specifically, interest rates affect buyer power.

External factors include:

- Rates: If rates rise, prices may soften.

- Jobs: Currently, tech growth drives demand.

- Inventory: When supply is low, prices spike.

Ms. San Francisco Real Estate tracks these daily. Thus, we know the right time to sell.

🏘️ 5. Comparable Sales (Comps)

Technically, this is how we find the number. Simply, we look at “comps.” These are recent sales nearby.

A good comp matches your:

- Size: Ideally, within 10% of your square footage.

- Age: Also, similar build dates.

- Distance: Preferably, within 0.5 miles.

However, adjustments are made. For instance, we add value for a view. Then, we subtract for a busy street. Ultimately, the data tells the truth.

💎 6. Special Features

Finally, the “X-factors” count. In San Francisco, certain traits are rare. Therefore, buyers pay extra for them.

High-value features:

- Views: Especially of the bridge or bay.

- Parking: Undoubtedly, a garage adds massive value.

- Tech: Increasingly, smart homes are preferred.

If you have parking, you win. Consequently, your appraisal will reflect that.

❓ FAQs: SF Home Values

How much does an appraisal cost? Typically, between $400 and $700. It depends on the size.

Can I increase my value before selling? Yes. Focus on kitchens and paint. Also, clean up the yard.

Do cash offers change the value? No. Appraisers look at the market value. However, cash closes faster.

Does a view really matter? Absolutely. In SF, a view can add 20% or more.

Final Thoughts

In summary, value is a mix of art and science. However, you don’t have to guess. Ms. San Francisco Real Estate is here to guide you. So, contact us for a professional estimate today.

How Investors Use Appraisals to Flip Homes in San Francisco (2026)

How Investors Use Appraisals to Flip Homes in San Francisco

Author: Ms San Francisco Real Estate | Last Updated: February, 2026

Currently, house flipping is a science. In San Francisco, the stakes are high. Therefore, guessing is dangerous. Instead, smart investors use data. Specifically, they use appraisal logic.

Basically, you must know the value before buying. Otherwise, you risk your cash. Fortunately, Ms. San Francisco Real Estate helps. We crunch the numbers. Below is your guide for 2026.

📐 1. The Magic Number: ARV

First, calculate the ARV. Simply, this is “After Repair Value.” Crucially, it predicts the future price.

Investors use ARV to decide:

- Price: Exactly what to pay today.

- Budget: How much to spend on repairs.

- Profit: What is left over.

To find this, we look at “comps.” Specifically, we find renovated homes nearby. Then, we compare them to your project. If you skip this, you fail. Thus, accuracy is key.

🧠 2. Think Like an Appraiser

Next, adopt the appraiser’s mindset. Before offering, analyze the deal. In fact, do the math yourself.

The Investor Checklist:

- Comps: First, find three closed sales.

- Condition: Next, compare the quality.

- Adjustments: Then, subtract for differences.

- Timing: Finally, check market trends.

Consequently, you find the “Max Allowable Offer.” Effectively, this prevents overpaying. So, you buy with a margin.

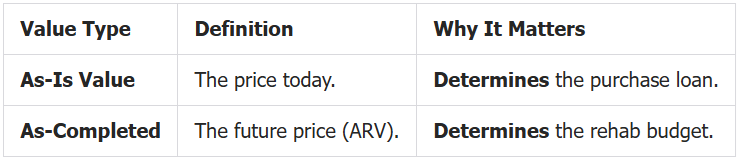

🏗️ 3. As-Is vs. As-Completed

Importantly, lenders see two numbers. Often, this confuses beginners.

Typically, hard money lenders need both. Therefore, your plan must be clear. If the spread is small, they say no. Thus, the math must work.

🛠️ 4. Bankable Renovations

Surprisingly, not all upgrades add value. Appraisers focus on function. Therefore, avoid personal tastes. Instead, focus on ROI.

What Appraisers Reward:

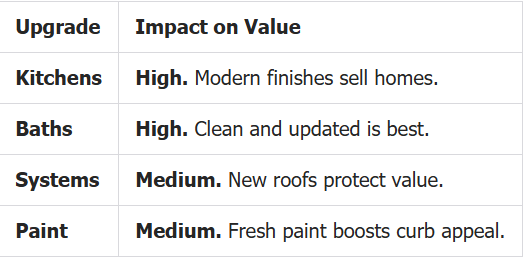

- Kitchens: Always update cabinets.

- Baths: Simply, make them modern.

- Systems: Crucially, fix the roof.

- Flooring: Ideally, keep it consistent.

Conversely, over-customization hurts value. So, keep it neutral.

📍 5. Neighborhood Strategy

Notably, San Francisco is patchy. In fact, values change by the block. Hence, your strategy must adapt.

- Condos: Here, HOA health matters.

- Houses: There, lot size matters.

- Location: Always, check the micro-market.

Proudly, Ms. San Francisco Real Estate prevents mistakes. Specifically, we stop “over-improving.” As a result, you save money.

🚪 6. The Exit Strategy

Eventually, you must sell. Usually, the buyer needs a loan. Consequently, the bank sends an appraiser. This is the final test.

If the appraisal is low:

- Option A: You lower the price.

- Option B: You offer credits.

- Option C: You challenge the report.

However, prevention is best. By pricing correctly, we avoid risks. Ultimately, the deal closes fast.

📈 7. Market Trends

Constantly, the market shifts. Appraisers watch the data. So, you should too.

Watch these metrics:

- Days on Market: If it rises, be careful.

- List-to-Sale Ratio: If it drops, lower offers.

- Inventory: If it spikes, competition grows.

Currently, we track this daily. Thus, you are never surprised.

❓ FAQs: Flipping & Appraisals

What is ARV? Simply, it is “After Repair Value.” It is your target.

Do I need an appraisal? Not always. However, your buyer usually does.

Which renovations pay off? Typically, kitchens and baths. Also, structural repairs.

Can a low appraisal kill a flip? Yes. If financing fails, the deal dies.

Final Thoughts

In summary, flipping requires precision. However, you can succeed. Ms. San Francisco Real Estate has the data. So, contact us today.

Top 10 San Francisco Zip Codes with Highest Appraisal Values (2026)

Top 10 San Francisco Zip Codes with the Highest Appraisal Values

Author: Ms San Francisco Real Estate | Last Updated: January, 2026

Currently, real estate is hyper-local. In San Francisco, this is especially true. Therefore, your zip code dictates your value. In fact, two neighbors can have different prices. Why? Because the zip code boundary matters.

Frequently, clients ask us a question. Specifically, “How much is my home worth?” Usually, the answer starts with five digits. Thus, your location is the baseline.

Proudly, Ms. San Francisco Real Estate guides you. Consistently, we help you understand the map. Below is the 2026 list of top-performing zip codes.

🗺️ How Zip Codes Drive Appraisals

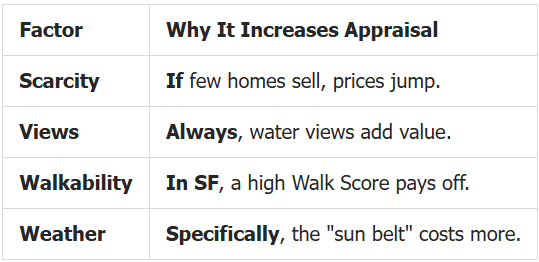

First, understand the math. Basically, appraisers use zip codes to find “comps.” Specifically, they look for similar sales nearby.

Key factors include:

- Scarcity: If homes are rare, value rises.

- Views: Undoubtedly, a bridge view adds value.

- Schools: Often, good schools boost prices.

- Walkability: In SF, buyers pay for convenience.

Consequently, the zip code sets the floor. Then, your home’s condition sets the ceiling.

🏆 The Top 10 High-Value Zip Codes

Here are the heavy hitters. Consistently, these areas appraise highest.

1. 94123 – Marina District

Visually, this area is stunning. Therefore, demand is huge. Typically, buyers love the Palace of Fine Arts. Also, they love the flat streets. Thus, condos here sell for a premium.

2. 94115 – Pacific Heights

Widely, this is the “Gold Coast.” In fact, it is the most prestigious zip. Here, you find mansions. Also, you find sweeping bay views. Consequently, appraisals are massive.

3. 94118 – Presidio Heights

Quietly, this area holds value. It sits near the park. Typically, families love the calm streets. Therefore, prices remain very stable.

4. 94121 – Sea Cliff

Uniquely, this is a beachside enclave. Here, homes sit on cliffs. Because inventory is low, prices stay high. Indeed, ocean views drive the numbers.

5. 94110 – Mission Dolores

Culturally, this is the heart of the city. Currently, tech buyers love it. Specifically, they want walkability. Also, they want the weather. Thus, modern condos appraise well here.

6. 94114 – Noe Valley

Consistently, this is a family favorite. It feels like a village. Therefore, resale value is excellent. Appraisers see this as a safe bet.

7. 94109 – Russian Hill

Iconically, this is San Francisco. Here, you have cable cars. Also, you have views. However, parking is tight. If you have a garage, value spikes.

8. 94108 – Nob Hill

Historically, this is old money. Today, it is a mix. Appraisals depend on the building. Specifically, luxury condos do best here.

9. 94131 – Glen Park

Surprisingly, this is a hidden gem. It feels like the suburbs. However, it has a BART station. Therefore, commuters pay top dollar.

10. 94116 – Outer Sunset

Recently, this area heated up. Why? Because it offers value. Also, it is near the beach. Consequently, appraisals are rising fast.

📊 What Drives the Value?

To clarify, here is a breakdown. Appraisers look for these traits.

💡 Buying in High-Value Zips

If you buy here, be ready. Competition is fierce.

- Expect Gaps: Often, the price exceeds the appraisal.

- Check Comps: Always verify the price.

- Cash Helps: Frequently, cash wins the deal.

Ms. San Francisco Real Estate protects you. We analyze the data first.

💰 Selling Strategy

Conversely, if you sell, be smart. You must defend your price.

Our Strategy:

- Document: First, list every upgrade.

- Price: Then, set a realistic number.

- Prepare: Finally, fix deferred maintenance.

By doing this, we justify the high appraisal.

🔗 Trust and Authority

Undoubtedly, local knowledge is key. We are Designated Local Experts™. Effectively, this means we know the zip codes. Google recognizes this expertise.

❓ FAQs: Zip Codes & Appraisals

Do zip codes really matter? Yes. Absolutely, they set the baseline price.

Can similar homes have different values? Yes. If the zip code changes, value changes.

Which zip is best for stability? Typically, 94115 (Pac Heights) and 94114 (Noe Valley).

Do condos appraise differently? Yes. Specifically, HOA health matters more.

Final Thoughts

In summary, location is power. However, you need a guide. Ms. San Francisco Real Estate knows the map. So, contact us today to maximize your investment.

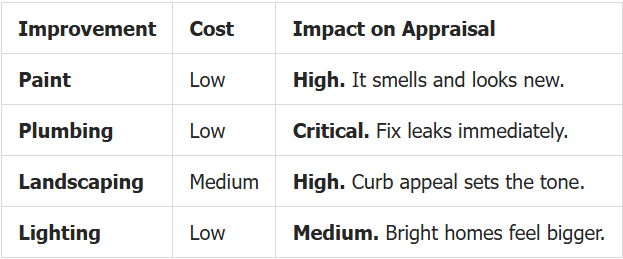

Top Renovations That Boost Appraisal Value in San Francisco

Top Renovations That Boost Appraisal Value in San Francisco

Author: Ms San Francisco Real Estate | Last Updated: January, 2026

Currently, the San Francisco market is unique. In fact, value is not just about size. Instead, appraisers look for condition. Therefore, the right upgrades matter.

However, mistakes are costly. If you choose wrong, you lose money. Fortunately, Ms. San Francisco Real Estate is here. We help you pick the winners. Below is your guide to high-ROI renovations in 2026.

🧐 How Appraisers Think

First, understand the process. Basically, appraisers compare sales. Then, they make adjustments. Specifically, they look for:

- Condition: Is the finish quality high?

- Layout: Does the flow work?

- Durability: Will the upgrades last?

- Market Fit: Does it match the neighborhood?

Ultimately, they prefer essentials. Thus, avoid over-customization.

🚀 1. Kitchens: The Value King

Undoubtedly, kitchens drive value. However, do not overspend. Simply, make it feel current.

What Appraisers Love:

- Cabinets: Just paint them or re-face them.

- Counters: Preferably, use stone or quartz.

- Appliances: Ensure they are energy-efficient.

- Lighting: Always brighten the space.

Conversely, avoid ultra-luxury items. Usually, they do not pay off.

🛁 2. Bathrooms: The “Move-In Ready” Signal

Next, focus on bathrooms. In fact, they rank second. Why? Because they signal good maintenance.

High-ROI Updates:

- Vanities: Instantly, a new unit adds style.

- Lighting: Also, update the fixtures.

- Mirrors: Simply, swap old for modern.

- Ventilation: Crucially, prevent mold.

As a result, the home feels “turnkey.” Thus, the value rises.

🛠️ 3. Deferred Maintenance

Surprisingly, boring fixes matter most. If you ignore them, value drops. Therefore, fix the basics first.

Must-Fix Items:

- Leaks: Immediately, fix water damage.

- Roofs: Always repair issues here.

- Windows: Specifically, fix broken seals.

- Safety: Also, repair loose railings.

By doing this, you avoid penalties. Consequently, the appraisal stays high.

⚡ 4. Energy Efficiency

Increasingly, SF buyers want efficiency. Therefore, upgrade your systems. In 2026, this is huge.

Appraiser Favorites:

- Windows: Ideally, install dual panes.

- Heat: Consider a modern heat pump.

- Insulation: Simply, keep the heat in.

As a result, bills go down. Thus, buyer interest goes up.

🏡 5. Curb Appeal

Visually, the exterior counts. Instantly, it sets the tone. So, make a good first impression.

Fast Wins:

- Paint: Freshly paint the exterior.

- Door: Also, update the front hardware.

- Garden: Simply, clean up the yard.

- Lights: Finally, add exterior lamps.

Effectively, this boosts the “condition rating.”

🪵 6. Flooring

Finally, check the floors. Ideally, they should be consistent. Also, they must be clean.

Best Choices:

- Hardwood: Specifically, refinish existing wood.

- Engineered: Alternatively, install durable wood.

- Carpet: If it is old, replace it.

Ultimately, consistent flooring wins. It makes the home feel larger.

⚠️ Renovations to Avoid

Conversely, some upgrades fail. Usually, they cost more than they add.

Use Caution With:

- Pools: Rarely, these add value in SF.

- Luxury: Often, ultra-custom finishes fail.

- No Permits: Legally, unpermitted work is risky.

Therefore, stick to the basics.

📍 Neighborhood Strategy

Notably, location changes things. Ms. San Francisco Real Estate tailors the plan.

- Noe Valley: Here, focus on layout and light.

- Sunset: Instead, focus on efficiency.

- SoMa: Mainly, focus on interior condition.

Thus, match the upgrade to the area.

⚖️ Renovate or Sell As-Is?

Sometimes, selling as-is is better. Before you build, calculate.

We Help You Compare:

- Cost: How much is the work?

- Value: How much will it add?

- Time: How long will it take?

Then, we decide. Sometimes, a cash offer is smarter.

❓ FAQs: Renovation Value

What adds the most value? Typically, kitchens and baths win. However, maintenance is key.

Do I need permits? Yes. Without them, appraisers may ignore the work.

Should I renovate before the appraisal? Yes. Start with the essential repairs.

What if I want to sell fast? Then, skip the big renovations. Instead, focus on cleaning.

Final Thoughts

In summary, be strategic. Only do work that pays off. Ms. San Francisco Real Estate knows the math. Contact us today to maximize your value.